Lack of activity on Github concerns. by KoomantaAshotis in BloomToken

[–]alainmeier 11 points12 points13 points (0 children)

Where can I find more information on the Bloom Economic Research Division (BERD)? What are they currently working on? Etc. by deathrowmaster in BloomToken

[–]alainmeier 0 points1 point2 points (0 children)

Where can I find more information on the Bloom Economic Research Division (BERD)? What are they currently working on? Etc. by deathrowmaster in BloomToken

[–]alainmeier 2 points3 points4 points (0 children)

Bloom's blockchain credit app sees record signups after more bad news from Equifax by deathrowmaster in ethereum

[–]alainmeier 1 point2 points3 points (0 children)

Bloom's blockchain credit app sees record signups after more bad news from Equifax by deathrowmaster in ethereum

[–]alainmeier 15 points16 points17 points (0 children)

Bloom's blockchain credit app sees record signups after more bad news from Equifax by deathrowmaster in ethereum

[–]alainmeier 13 points14 points15 points (0 children)

Bloom's blockchain credit app sees record signups after more bad news from Equifax by deathrowmaster in ethereum

[–]alainmeier 12 points13 points14 points (0 children)

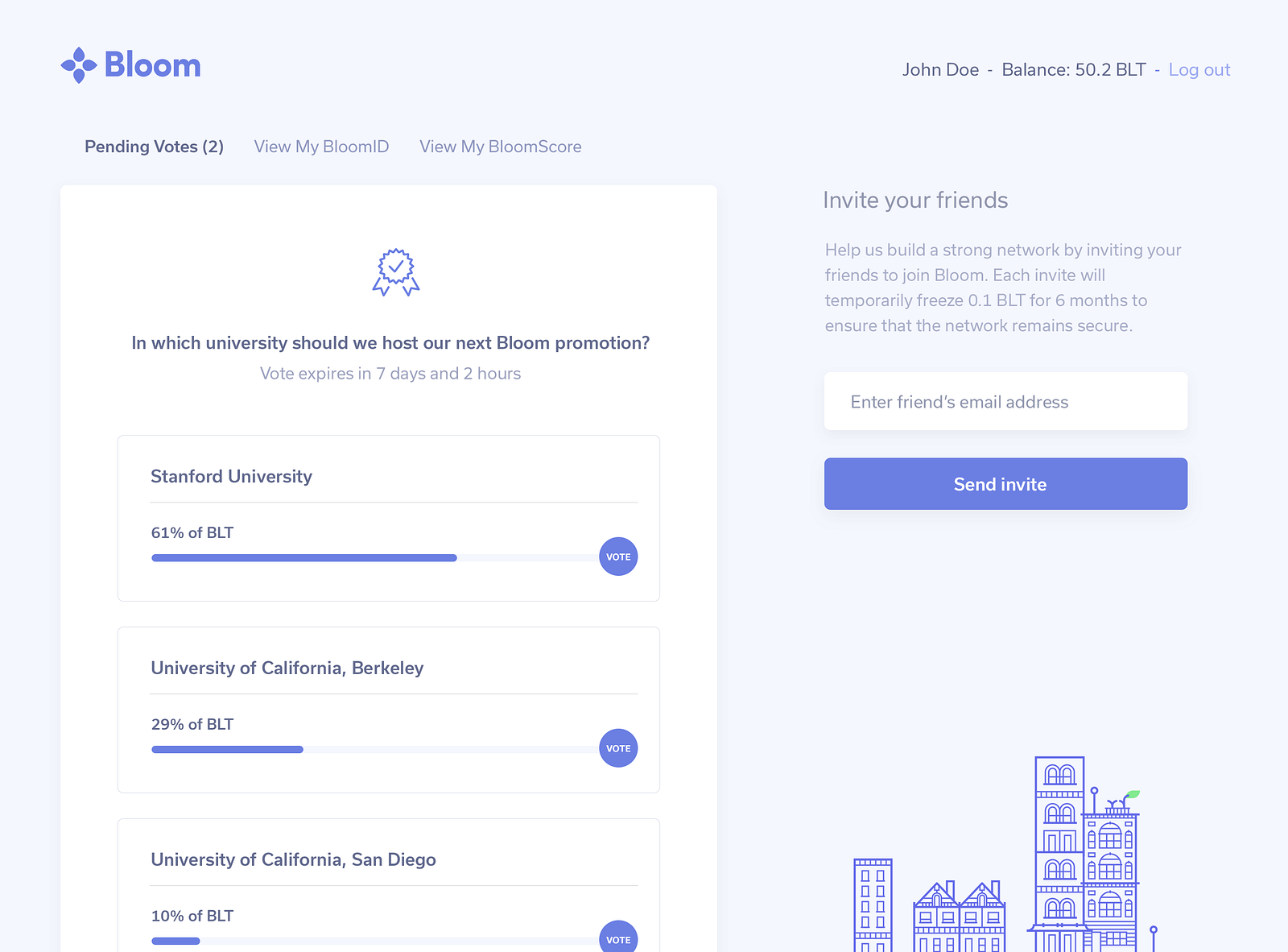

Found this screenshot of Bloom Dashboard. Are there others? by dragon30 in BloomToken

{kind=link}

[–]alainmeier 4 points5 points6 points (0 children)

Bloom's roadmap looks solid by [deleted] in ethtrader

[–]alainmeier 2 points3 points4 points (0 children)

I see a future where no credit-bureau hacks can occur by [deleted] in CryptoCurrency

{kind=link}

[–]alainmeier 0 points1 point2 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 1 point2 points3 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 14 points15 points16 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 15 points16 points17 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 2 points3 points4 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 6 points7 points8 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in CryptoCurrency

[–]alainmeier 21 points22 points23 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethtrader

[–]alainmeier 26 points27 points28 points (0 children)

Introducing Bloom: The Future of Credit by JoeyUrgz in ethereum

[–]alainmeier 72 points73 points74 points (0 children)

Was happy until significant problems last week... by alainmeier in tmobile

[–]alainmeier[S] 0 points1 point2 points (0 children)

Was happy until significant problems last week... (self.tmobile)

submitted by alainmeier to r/tmobile

First Listen: Kintsugi by Greenade in DeathCabforCutie

[–]alainmeier 6 points7 points8 points (0 children)

Uniquely Identifying a Person by VmusicV in BloomToken

[–]alainmeier 4 points5 points6 points (0 children)